Understanding Know Your Customer (KYC)

Know Your Customer (KYC) ensures that financial institutions verify customer identities. This process helps prevent fraud, money laundering, and other financial crimes. Banks and businesses must follow KYC regulations before establishing relationships with clients.

KYC requirements vary by country, but most include identity verification and risk assessment. Authorities enforce these regulations to create a secure financial environment. Additionally, KYC compliance builds trust between institutions and customers.

Components of a KYC Form

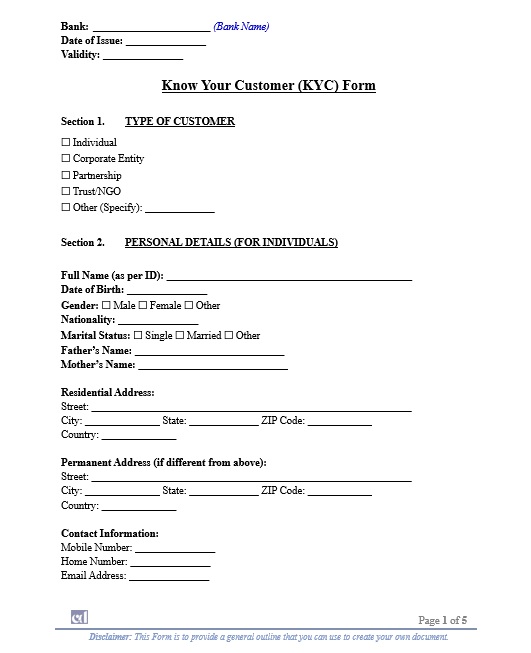

A standard KYC form collects essential customer details. It includes personal information like name, date of birth, and residential address. Customers must also provide valid identification, such as a passport or driver’s license.

Financial institutions may request additional details for high-risk clients. These details include occupation, income source, and financial history. Providing accurate information ensures compliance and smooth transactions.

Why KYC Is Essential for Businesses

Businesses implement KYC to reduce financial risks. Verifying customer identities prevents fraudulent transactions and unauthorized access. Additionally, KYC ensures adherence to anti-money laundering (AML) laws.

Failure to follow KYC regulations can lead to penalties and legal issues. Therefore, companies must update customer information regularly. This practice helps maintain accurate records and strengthens security.

Challenges in KYC Compliance

KYC compliance requires continuous updates and verification. Customers often find the process time-consuming, especially with strict documentation requirements. However, financial institutions must follow these measures to maintain regulatory compliance.

Advancements in digital KYC solutions help simplify verification. Many organizations now use biometric authentication and AI-driven checks. These innovations speed up the process while ensuring security.

Conclusion

KYC is a vital process that safeguards financial institutions and businesses from fraud, money laundering, and other financial crimes. By verifying customer identities and assessing risk, KYC ensures compliance with regulatory standards while fostering trust between institutions and clients. Although the process can be complex and time-consuming, advancements in digital KYC solutions are making verification more efficient and secure. Businesses must remain proactive in updating customer information to maintain compliance and mitigate risks. Ultimately, KYC is essential for creating a safer and more transparent financial environment.

References

- Financial Action Task Force (FATF) – www.fatf-gafi.org

- International Monetary Fund (IMF) – www.imf.org

- Bank for International Settlements (BIS) – www.bis.org

has been added to your cart!

have been added to your cart!